With the world of finance undergoing massive changes and facing expansion, paper-based currencies are slowly reducing their worthiness. Besides damaging the environment and contributing towards the generation of black money, it serves no other purpose.

It was about time to introduce a new set of currency that is environment-friendly and has some accountability. This revolution in the finance market has led to the introduction of Digital Currency.

Today we will explore CBDCs, how they work, why they matter, and what challenges & opportunities they pose for the future of finance.

What is Central Bank Digital Currency (CBDC)?

CBDC is a digital currency that is a form of digital currency issued by the country’s central bank. Unlike physical cash or bank deposits, CBDCs are controlled by the central bank and have the sole authority over it. CBDCs are not to be confused with Bitcoin & Ethereum which are decentralised and not in control of any regulatory body. You can simply understand CBDCs as a complete replica of physical currency but in a digital format with somebody to oversee the transactions.

CBDCs are classified into two types: Wholesale and Retail.

Interbank transactions and settlements are performed using wholesale CBDCs whereas transactions between customers and merchants are performed using retail CBDCs. Wholesale CBDCs have been present in the market for decades but the concept of retail CBDCs is new that aims to provide the public with access to digital bank money.

How do CBDCs work?

Since the Central Bank Digital Currency is issued by the central bank, the usage pattern remains moreover same.

Issuance by Central Bank

The central bank creates and issues CBDCs as per the monetary policy objectives and rules. Moreover, it determines the supply and distribution of CBDCs along with their interest rate & exchange rate.

Account Setup

To start using CBDCs, everyone needs to have an account in any one of the licensed banks and register themselves for the CBDC programme. In India, the CBDC programme i.e., e-rupee is in the trial phase. So, users need to download their bank's respective CBDC app and start loading their wallet with the digital currency.

Transaction Initiation

Individuals or businesses can initiate transactions using CBDCs through their banking app and pay for the services from their digital wallet.

Verification

When a CBDC transaction is initiated, the central bank or the licensed banks verify the authenticity of the transactions. The verification process ensures that the CBDC that is being transferred is not a counterfeit or double-spent.

Transfer

Once the transaction is verified, the digital note is transferred to the recipient’s account. This transfer occurs electronically and is recorded in a secure ledger maintained by the central bank and other trusted parties.

Ledger Maintenance

Every CBDC transaction is recorded on a digital ledger tracking the ownership and movement of the currency. Since the ledge is centralised, its value is fixed, unlike other cryptocurrencies.

Why CBDC is important?

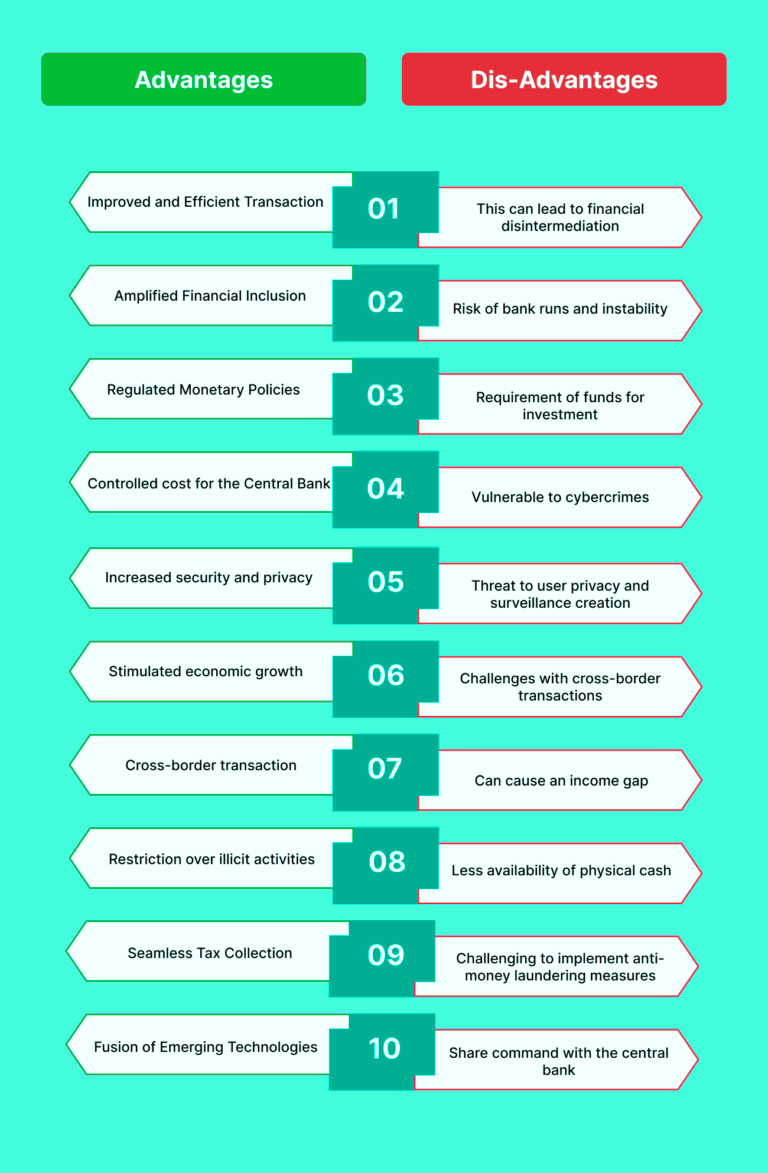

CBDCs have several benefits over physical currency such as:

CBDCs can reduce financial exclusion by providing access to digital central bank money to anyone with smart devices. Additionally, it can tap into millions of underbanked and unbanked populations to participate in the digital revolution and benefit from financial services.

It improves the efficiency and speed of financial transactions by reducing intermediation costs, frictions and delays. Furthermore, it contributes towards an eco-friendly method of transaction eliminating the cost of producing paper currency.

CBDC enhances the convenience and user experience of financial services of the user, It provides the user with ample choices, flexibility and functionality.

Digital currency is an innovative technology to counter the use of paper currencies along with tracking and outing black money. Since the ledger is maintained and overseen by the central bank, evading taxes is next to impossible.

Conclusion

CBDC is a pilot programme that holds the potential to change the traditional financial system. Every new system suffers from major drawbacks but with innovation & development users can adapt to the changing financial ecosystem. The digital currency has been adopted by most countries and is going to transform the entire fintech ecosystem.