The global fintech market is on a first-rate trajectory, having reached a staggering value of about $194.1 billion in 2022. What’s even more interesting the annual growth rate of the fintech industry stands at 16.8%, soaring new heights. Moreover, the global fintech market is anticipated to cross $ 492.81 billion by 2028 with the forthcoming of new technologies & innovation in the fintech market.

The Need for Fintech:

Naturally, you might be wondering: Why fintech when traditional banks exist?

For those who are aware of the world of banking, the answer lies within the shortcomings of conventional banking institutions. Regular banks often have a slow process, operational inefficiencies and persistent long-resolution times extending to months. Additionally, a major portion of banking services remain active for offline operations. To tackle these issues and give customers a more convenient solution, there was a strong need for change in the financial sector which was served by fintech industries.

The Rise of Fintech

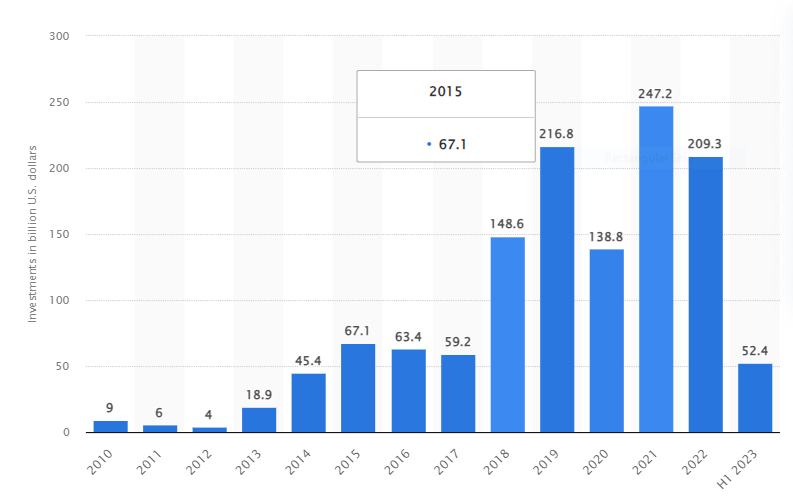

The fintech industry has witnessed an unprecedented boom during the last decade. As per Statista, international fintech investment reached approximately $247.2 billion in 2021. The meteoric rise can be attributed to several factors increasing the adoption of smartphones, rising demand for digital payment solutions and the emergence of blockchain technology.

The Fintech Challenge

With the emergence of fintech corporations and the creation of a diverse range of fintech products, banks have been trying to stay at par with these companies. This direct competition has forced banks to harness the technological prowess of fintech, ushering in a transformative segment that promises enhanced efficiency & swiftness; thereby revolutionising the entire banking landscape.

The Fintech Transformation

Now let’s dive deep into how fintech can accomplish this remarkable transformation and create unattainable value for both customers & businesses:

1. Enhancing Financial Inclusion

One of the most critical impacts of fintech on banking is its capability to promote financial inclusion. Traditional banks have often struggled to attain underserved and unbanked populations. This led fintech companies to leverage mobile technology and innovative payment platforms to provide financial services to previously excluded individuals, thus bridging the gap between the banked and unbanked. Thus, bridging the gap between the banked and the unbanked.

2. Efficiency and Automation

Fintech solutions are revolutionising the way banking operations are being carried out. Automation i.e., powered by artificial intelligence and machine learning, is streamlining the processes like customer onboarding, credit underwriting and fraud detection. This not only reduces operational costs for banks but also leads to efficient & more accurate services for customers.

3. Convenience and Digital Banking

The rise of fintech has given birth to virtual banks or neo-banks operating exclusively online. These digital banks offer customers a seamless & user-friendly banking experience with convenient services like opening instant savings accounts to avail of personal loans. The simplicity and elegance of a finance management system through a smartphone app has attracted a new generation of tech-savvy customers.

4. Innovation in Lending

Fintech has migrated the lending market to a completely digital domain. Peer-to-peer lending systems and online marketplaces are connecting borrowers with investors, eliminating the need for traditional intermediaries. Additionally, fintech-driven algorithms are leveraging alternative information sources to assess creditworthiness, making it less complicated for individuals and small groups to get entry to loans.

5. Blockchain and Cryptocurrency

Blockchain technology, which underpins cryptocurrencies like Bitcoin, holds the potential to disrupt conventional banking in profound approaches. Blockchain provides secure, transparent and tamper-proof transaction records that reduce the risk of fraud and improve the efficiency of cross-border payments. Additionally, some of the banks are also exploring the issuance of digital currencies in the wake of rising popularity among consumers & stakeholders.

6. Regulatory Challenges and Collaboration

While fintech affords numerous opportunities, it additionally possesses regulatory challenges. Hence regulators like central banks must strive to find a balance between fostering innovation and protecting consumers. The joint effort among fintech corporations, traditional banks and regulators has become essential to create a regulatory framework guaranteeing monetary stability and promoting consumer safety.

7. Customer-Centric Solutions

Fintech has placed a robust emphasis on client-centric solutions i.e., promoting personalisation. It is the key, as fintech companies are leveraging data analytics to understand customer behaviour and preferences. Moreover, this data-driven approach allows banks to tailor their products and services to individuals' needs which provides them a more satisfying customer experience.

Conclusion

The future of banking is undeniably intertwined with the evolution of fintech. With the rapid advancement of technologies, we will be witnessing more groundbreaking innovations in the financial service sectors. Fintech is just shaping the future of banking; it’s redefining it i.e., making it more accessible, efficient and customer-centric than ever before. In this dynamic landscape where collaboration and innovation are the only true mantra to success, banks & fintech's must join hands to forge an ever-lasting partnership catering to businesses and customers.